Here are four tactics that could help you get your tax bills under control.

Taxes are complicated, but if you get behind on paying them, things can get even more complicated — and quickly. If you owe back taxes, here are four common options that could help you find some tax relief, plus guidance on how many years can you file back taxes and how to file back taxes.

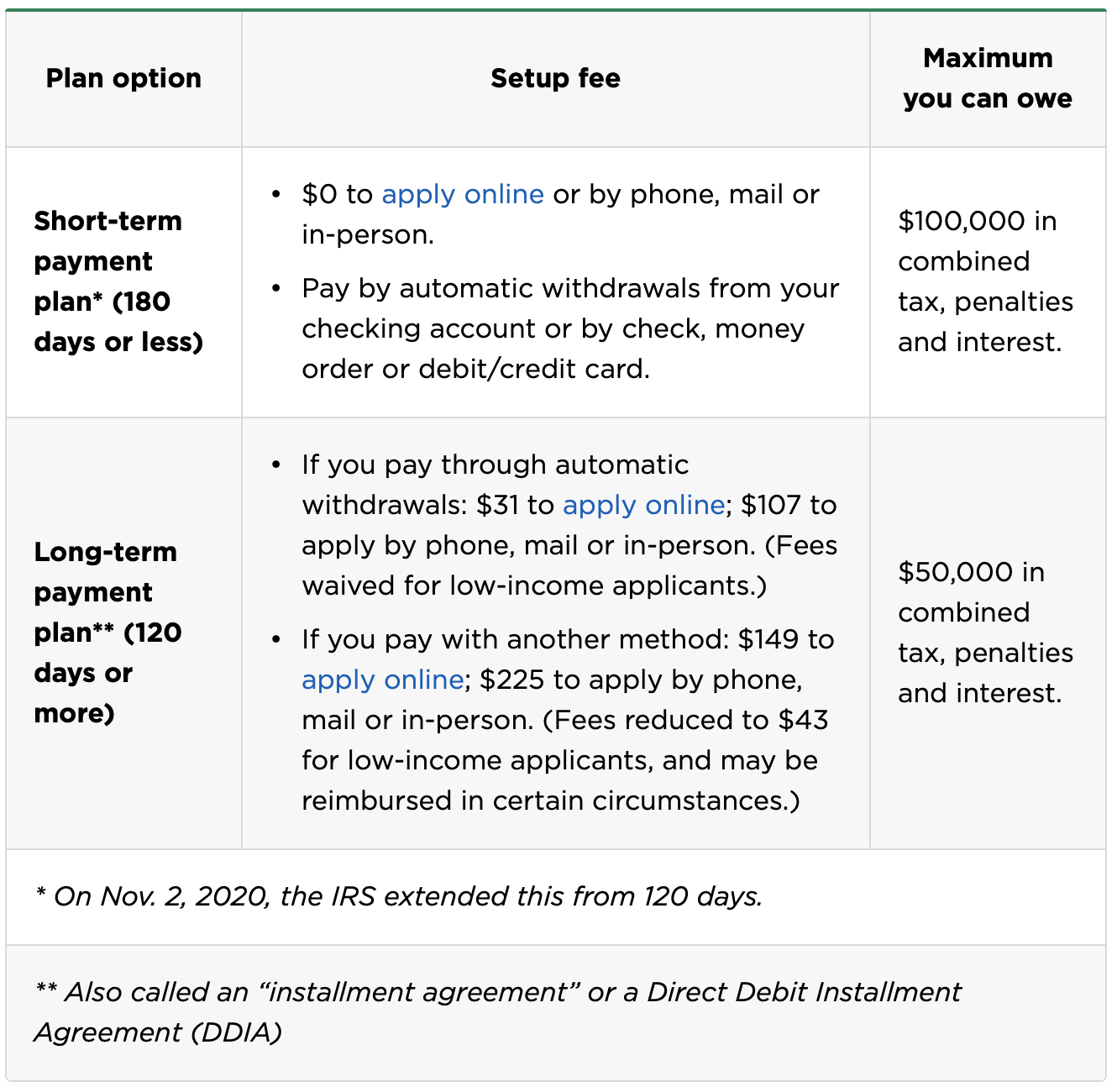

1. IRS payment plans

If you need more time to pay your tax bill, the IRS will probably give it to you in the form of a payment plan.

The IRS offers two types of installment plans (learn more about IRS payment plans here).

Here are a few things to know about getting tax relief via an IRS payment plan:

-

A payment plan doesn’t get you out of interest and penalties for late payment. Those accrue until your balance is zero.

-

If you owe more than $25,000, you have to make your payments via automatic withdrawals from a bank account.

-

If you make your payments with a debit or credit card, you'll have to pay a processing fee (the charge for debit cards runs about $2-$4 per payment; the charge for credit cards is about 2% of the payment).

-

"Low-income applicant" generally means your adjusted gross income is at or below 250% of the federal poverty level. You can see if you qualify on IRS Form 13844.

-

As part of the government's ongoing coronavirus response, people who already have installment agreements did not have to make payments due between April 1 and July 15, 2020. The IRS also said it wouldn't deem any installment agreements in default during that period, but interest would still accrue on unpaid balances.

» MORE: Here's a list of ways to send money to the IRS

2. Offers in compromise

You might be able to find tax relief through what’s called an "offer in compromise." This lets you settle your back taxes with the IRS for less than you owe. According to the IRS, it may be an option if you absolutely can’t pay your tax debt or if doing so creates a financial hardship.

But it's much harder to get the IRS to sign off on an offer in compromise than on a payment plan. The IRS accepts fewer than half the requests. You should explore other options before turning to an offer in compromise.

To determine whether you qualify for tax relief via an offer in compromise, the IRS considers your ability to pay, your income and expenses, and how much you have in assets.

APPLYING FOR AN OFFER IN COMPROMISE

The materials and instructions for submitting an offer in compromise are in IRS Form 656-B. Here are a few things to know:

-

There’s a $205 fee, and it's nonrefundable (low-income taxpayers can get a waiver).

-

You’ll also need to make an initial payment, and it’s nonrefundable as well.

-

You have to be current on all your tax returns. If you haven’t filed a tax return in a while, you may not qualify.

-

The IRS can file or keep tax liens in place until it accepts your offer and you’ve fulfilled your end of the deal.

-

You don’t qualify if you are in an open bankruptcy proceeding.

-

You can hire a qualified tax professional to help you do the paperwork, but it’s not required.

-

Once you file your application, the IRS suspends collection activities.

IF THE IRS ACCEPTS YOUR OFFER

-

Your initial payment has to be either 20% of what you’re offering to pay (if you're paying in five or fewer installments) or your first monthly installment (if you're paying in six or more monthly installments).

-

Be aware that some of the information about your offer in compromise could be made public. The IRS’ public inspection files on offers in compromise include the taxpayer's name, city, state, ZIP code, liability amount and offer terms.

-

Any federal tax liens the IRS has filed against you don't go away until you’ve fulfilled your end of the deal.

If the IRS rejects your offer, you can appeal within 30 days. The agency has an online self-help tool to walk you through that.

3. 'Currently Not Collectible' status

If you can't pay your taxes and your living expenses, within reason, you can ask the IRS to put your account in what’s called "Currently Not Collectible" status. You need to request this delay in collection, and the IRS may ask you to complete a Collection Information Statement to prove that your finances are as bad as you say they are. You'll need to supply information about your monthly income and expenses on that form.

Here are some things to know about this form of tax relief:

-

It's temporary — the IRS may review your income annually to see if your financial situation has improved.

-

Being deemed "Currently Not Collectible" doesn't make your tax debt go away.

-

The IRS can still file a tax lien against you.

4. Should I hire a tax relief company?

Tax relief companies typically offer to help taxpayers in distress. Some of them can be helpful if you’re confused about the process or need help filling out forms. But remember:

-

The IRS rejects most applications for offers in compromise.

-

If a tax relief company loses or delays your application, you’re still on the hook for your tax debt, interest and penalties with the IRS.

-

You may have to pay an upfront fee to the tax relief company, and it may be a percentage of the tax you owe. That fee may be higher than what you end up saving on your tax bill if the IRS accepts your offer in compromise (and it might not be refundable if the IRS rejects your offer).

-

Tread carefully, the Federal Trade Commission warns; there are some bad actors out there. "The truth is that most taxpayers don't qualify for the programs these fraudsters hawk, their companies don't settle the tax debt, and in many cases don't even send the necessary paperwork to the IRS requesting participation in the programs that were mentioned. Adding insult to injury, some of these companies don't provide refunds, and leave people even further in debt," it says.

Some tax relief companies will charge you a fee to determine how much you owe the IRS, set up a payment plan or see if you qualify for an offer in compromise. But these and other things you can do yourself for free:

-

Find out whether you have a balance outstanding with the IRS and how much it is. You can get that (and up to 24 months of your payment history) at IRS.gov/account. Signing up takes about 15 minutes, and the IRS says you’ll only need to verify your identity once.

-

Get your tax records. The IRS provides five types of free tax transcripts that let you peek at its records on you. You can see most line items from your tax returns processed during the last three years, for example, or get basic data such as your marital status, how you paid and your adjusted gross income for the current tax year and for up to the last 10 years. (Note that a tax transcript isn’t the same as a copy of your tax return.)

-

Set up a payment plan with the IRS, as described above.

-

See if you qualify for an offer in compromise. You can use the IRS' online pre-qualifier tool to see if an offer in compromise might be for you. Remember, the tool is just the beginning of the journey — you'll still need to complete a formal application.

-

Tax relief in disaster situations

If you've been affected by a federally declared disaster such as a hurricane, the IRS may provide people in your region with an automatic extension to file and pay your taxes. Typically you're eligible if you live or have a business in the federally declared disaster area. You might also be able to deduct some of your personal property losses that are not covered by insurance or other reimbursements. The IRS maintains a list of the disaster situations for which it is offering tax relief.

How many years can you file back taxes?

You can file a tax return for any prior year, but the IRS typically requires taxpayers to file back tax returns for the last six years in order to avoid delinquency enforcement procedures. According to IRS policy, it takes managerial approval to go back more than six years.

How to file back taxes for multiple years

Here are three steps to follow:

-

Gather prior-year documents. You'll need tax documents for the year you're filing your tax return for (e.g., you'll need your W-2, 1099s or other documents from 2018 if you're filing your 2018 tax return). If you don't have those documents, you can request a tax transcript from the IRS for that year (here's how to do that). Although you won't get exact photocopies of the documents, you'll get the information contained in those documents, which is what you'll need to get your return done.

-

Use the right year's tax forms. Don't file a 2018 tax return using 2020 tax forms. Tax rules and tax forms are different every year. (Here are some important tax forms to know.)

-

Don't be afraid to ask for help. Tax rules change every year, and you'll need to ensure you're applying the right rules to the right year. Good news: Many tax software packages allow you to file prior-year tax returns.

-

What happens if you don't file taxes for several years?

Catching up on filing past-due tax returns seem like an overwhelming task, but are a few things in it for you.

-

It avoids the IRS doing it for you. This is called a substitute return. What basically happens is the IRS takes the information it has on hand for you, uses it to cobble together a tax return and sends you the bill. That may sound convenient, but actually it's almost always a guaranteed bigger headache. The IRS often doesn't know which tax deductions or tax credits you might have qualified for, leading to a bill higher than what you might've had if you'd done it yourself.

-

You can pay your tax bill in installments. Filing a tax return late and paying a tax bill late are two different things with two different sets of penalties. Don't avoid filing a tax return because you can't pay the bill. Again, the IRS offers several types of installment plans (and other payment programs) you can use to pay over time.

-

The government might owe you money. If you're due a tax refund for a prior year, claim it by filing your tax return for that year. Don't drag your feet; you only have three years from the original tax return due date to claim old tax refunds.

-

You can avoid problems getting a loan. Copies of current tax returns are a common requirement for getting mortgages and other loans.

Author, Orem. T. (2021, 03 03). Tax Relief: How to Get Rid of Your Back Taxes. Nerdwallet.

https://www.nerdwallet.com/article/taxes/tax-relief-back-taxes

About the author: Tina Orem is NerdWallet's authority on taxes. Her work has appeared in a variety of local and national outlets